Secure Your Future: Retirement Planning Guide

Welcome to SimpliWealth's Retirement Planning Guide. We understand that planning for retirement can be a daunting task, but it is a crucial step towards ensuring a comfortable and fulfilling life during your golden years. In India, where family ties are strong, securing your retirement is essential to avoid becoming financially dependent on your children and maintain your dignity and autonomy. In this comprehensive guide, we will walk you through the essential aspects of retirement planning and empower you to make informed decisions. Let's embark on this journey towards a financially secure future together!

Understanding the Importance of Retirement Planning

In India, the traditional focus on children's education and marriage often leads individuals to neglect their retirement planning. However, it is vital to recognize that retirement is a phase of life that requires careful consideration. By prioritizing retirement planning, you can:

Attain Financial Independence: Relying solely on children for financial support may lead to uncertainty and loss of independence. A well-planned retirement ensures you are self-reliant during your golden years.

Maintain Dignity and Autonomy: By securing your finances, you can make decisions that align with your preferences and lead a life of dignity without feeling like a burden on your loved ones.

Prepare for Healthcare Expenses: As you age, healthcare needs may increase. Adequate retirement planning can help you cover medical costs without straining your family's resources.

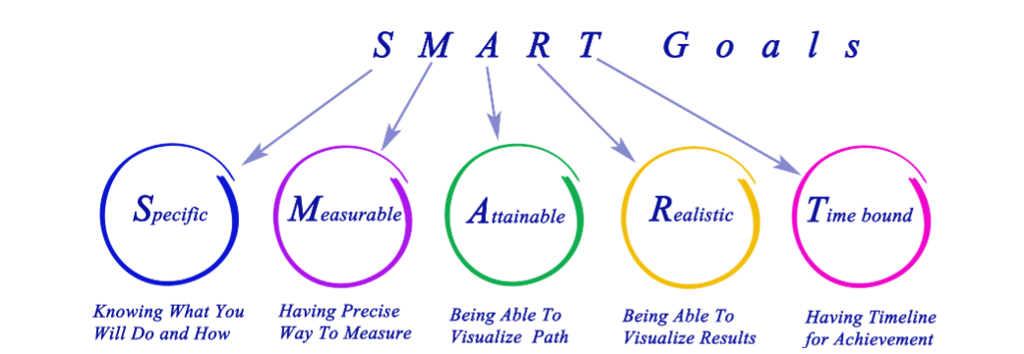

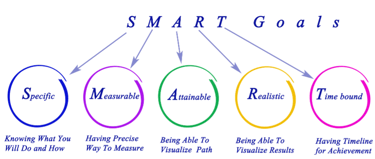

Setting Retirement Goals

As you journey towards a financially secure retirement, setting clear and realistic retirement goals is paramount. Envisioning your ideal retirement lifestyle empowers you to make informed decisions and formulate a comprehensive retirement plan. Calculate Required Savings: Understanding your retirement goals enables you to estimate the amount you need to save to achieve them.

Understanding Your Retirement Expenses:

To determine your retirement goals, you need to estimate your future expenses. Begin by assessing your current monthly expenses and considering factors that might change in retirement, such as housing, healthcare, and travel. Some expenses might decrease (e.g., work-related costs), while others could increase due to medical needs or leisure activities.

Calculating Required Savings:

Once you have an estimate of your annual retirement expenses, you can calculate the corpus required to sustain that lifestyle.

some general thumb rules can provide a quick estimate of the corpus you might need for a comfortable retirement:

The 4% Rule: According to this rule, you can withdraw approximately 4% of your retirement corpus annually without depleting it over a 30-year period. To apply this rule, divide your annual expenses by 0.04 (4%).

Assessing Your Current Financial Situation

Evaluating your current financial status is the foundation of effective retirement planning. Consider the following steps:

Create a Personal Balance Sheet: List your assets, including savings, investments, and property, as well as your liabilities, such as loans and mortgages.

Analyze Income and Expenses: Develop a budget to assess your cash flow and identify areas where you can save more for retirement.

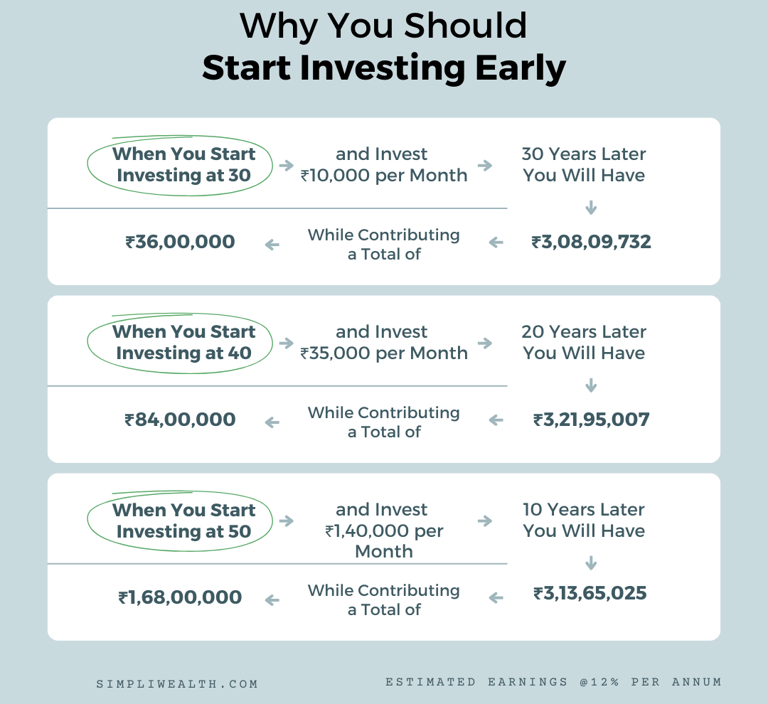

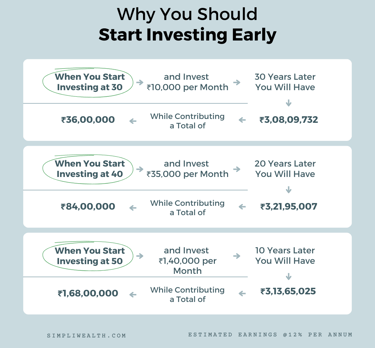

Starting Early: The Power of Compound Interest

In India, starting early is critical due to the power of compounding. Compounding allows your investments to grow exponentially over time. For instance:

The chart shows three scenarios:

Scenario 1: You start investing at age 30 and invest 10,000 Indian Rupees (INR) per month. After 30 years, you will have 3.08 crores INR, while contributing a total of 36,00,000 INR.

Scenario 2: You start investing at age 40 and invest 35,000 INR per month. After 20 years, you will have 3.21 crores INR, while contributing a total of 84,00,000 INR.

Scenario 3: You start investing at age 50 and invest 140,000 INR per month. After 10 years, you will have 3.13 crores INR, while contributing a total of 1.68 Crores INR.

As you can see, the earlier you start investing, the more time your money has to grow. This is because of the power of compound interest. Compound interest is when you earn interest on your interest. So, the longer your money is invested, the more interest it will earn.

Retirement Investment Options

India offers various retirement investment options with unique benefits. Some popular options include:

Provident Fund (PF)

The Provident Fund (PF) is a mandatory retirement savings scheme for all employees in India. It is a contributory scheme, where both the employee and the employer contribute a fixed amount each month. The money in the PF account is invested in government securities and earns a fixed interest rate.

The PF has several advantages, including:

It is a tax-deductible investment up to 1.5 lakh per annum under section 80C.

The interest earned on the PF money is tax-free.

The money in the PF account is safe and secure.

The PF account can be used to take a loan or to buy a house.

The average CAGR earnings of the PF have been around 8-9% over the past few years.

Public Provident Fund (PPF)

The Public Provident Fund (PPF) is a long-term investment scheme that offers tax benefits and attractive interest rates. The PPF is a non-market linked scheme, which means that the interest rate is fixed by the government.

The PPF has several advantages, including:

It is a tax-deductible investment up to a certain limit.

The interest earned on the PPF money is tax-free.

The money in the PPF account is safe and secure.

The PPF account can be opened by anyone, regardless of their income.

The average CAGR earnings of the PPF have been around 8% over the past few years.

National Pension System (NPS)

The National Pension System (NPS) is a voluntary retirement savings scheme that was introduced by the Government of India in 2004. The NPS is a market-linked scheme, which means that the returns on your investment will depend on the performance of the underlying assets.

The NPS has several advantages, including:

It offers a choice of investment options, so you can choose the option that is most suitable for your risk tolerance.

The returns on your investment are tax-free, up to a certain limit.

The money in your NPS account is safe and secure.

You can withdraw your money after you reach the age of 60, or you can use it to buy an annuity.

The average CAGR earnings of the NPS have been around 10% over the past few years.

Mutual Funds

Mutual funds are a type of investment vehicle that pool money from a group of investors and invest it in a variety of assets, such as stocks, bonds, and money market instruments. Mutual funds offer diversification and professional fund management, making them ideal for long-term growth.

There are many different types of mutual funds available, so it is important to choose one that is suitable for your investment goals and risk tolerance. Some of the most popular types of mutual funds for retirement include:

Equity funds: These funds invest in stocks, which offer the potential for higher returns but also higher risk.

Debt funds: These funds invest in bonds, which offer lower returns but also lower risk.

Hybrid funds: These funds invest in a mix of stocks and bonds.

The average CAGR earnings of mutual funds have been around 12% over the past few years.

Assessing Risk Tolerance

Understanding your risk tolerance is pivotal to aligning your investments with your comfort level. Here's how to navigate this crucial aspect:

Risk Profiles:

There are three main risk profiles:

Conservative: You prioritize safety and stability. You're comfortable with lower returns to protect your principal investment.

Moderate: You seek a balance between risk and return. You're open to some fluctuations in exchange for potential growth.

Aggressive: You're willing to take higher risks for the potential of greater returns. You can handle market volatility.

Investment Strategies:

Each risk profile corresponds to suitable investment strategies:

Conservative: Focus on low-risk instruments like fixed deposits and debt funds to preserve capital.

Moderate: Allocate to a mix of equities and fixed income instruments for balanced growth and stability.

Aggressive: Consider higher exposure to equities, including equity mutual funds, for potential high returns.

By gauging your risk tolerance, you can craft an investment strategy that aligns with your financial goals and emotional comfort. Remember, your risk profile can evolve, so regular evaluations are key to maintaining a suitable investment mix.

Tax Planning for Retirement

Effective tax planning is a vital component of preparing for retirement. Here's how you can optimize your tax strategy:

Tax-Deferred Accounts:

Explore retirement-specific investment avenues with attractive tax benefits, like the National Pension System (NPS). This account allows you to:

Save on Taxes: Contributions to NPS are eligible for tax deductions under Section 80C of the Income Tax Act.

Build Retirement Corpus: Your NPS investments grow over time, offering a substantial corpus upon retirement.

Flexibility in Withdrawals: NPS provides flexibility in withdrawing funds, ensuring a balanced financial journey post-retirement.

Tax-Free Investments:

Consider tax-free investment options such as tax-free bonds and equity-linked savings schemes (ELSS):

Tax-Free Bonds: Invest in bonds issued by government entities, enjoying tax-free interest income.

ELSS: These equity-linked savings schemes offer the twin benefits of potential equity growth and tax deductions under Section 80C.

By strategically utilizing these tax planning tools, you can maximize your retirement savings while minimizing your tax liabilities, securing a more prosperous retirement.

Regularly Review and Adjust Your Retirement Plan

Life is marked by its unpredictability, and circumstances can change without warning. Ensuring the continued effectiveness of your retirement plan requires vigilance and adaptation:

Periodic Assessments:

We strongly advise that you review your financial goals and investments at least annually, or more frequently when major life events occur. These assessments serve several crucial purposes:

Stay on Course: Regular evaluations enable you to ensure that your retirement plan aligns with your evolving objectives and current financial circumstances.

Adjust for Changes: Life's twists and turns may necessitate alterations to your retirement strategy. Periodic assessments let you adapt to unexpected developments.

Seize Opportunities: Market trends and investment options shift over time. Regular reviews help you capitalize on potential opportunities for growth.

By adopting a proactive approach to reviewing and adjusting your retirement plan, you're better equipped to navigate the ever-changing financial landscape and achieve your long-term retirement goals.

Retirement Income Sources

t's essential to know where your income will come from beyond your savings. Here are two key sources to consider:

Pensions:

Many employers offer pension plans to their employees. These plans provide you with a regular income after you retire. Here's what you need to understand:

Types of Pensions: There are different types of pension plans. Some give you a fixed amount based on your salary, while others depend on your contributions and investment growth.

Plan Details: Check the terms of your pension plan, including when you can start receiving payments and how they're calculated.

Reliable Income: Pensions ensure a reliable income stream throughout your retirement.

Annuities:

Annuities are another option. You pay a lump sum to an insurance company, and they provide you with a regular income in return:

Steady Payments: Annuities offer guaranteed payments, which can help you budget effectively.

Different Choices: There are various types of annuities, like those that continue payments to your spouse after you pass away.

Tax Benefits: Annuities often come with tax advantages, making them an appealing option for retirees.

Understanding these sources of retirement income can help you build a well-rounded financial plan for your golden years.

Healthcare and Long-Term Care Planning

Healthcare expenses are a significant consideration when planning your retirement in India. Here's how you can ensure your healthcare needs are covered:

Health Insurance:

Having comprehensive health insurance is crucial to managing medical costs during retirement:

Health Coverage: Ensure your health insurance covers various medical services, hospitalization, and treatments.

Preventive Care: Look for policies that include preventive care, as staying healthy can save you costs in the long run.

Family Inclusion: Some policies allow including family members, providing broader coverage.

Conclusion

In conclusion, prioritizing retirement planning in India is crucial to enjoy financial independence, dignity, and a comfortable lifestyle during your golden years. By following the steps outlined in this guide, you can create a robust retirement plan tailored to your goals and risk tolerance. SimpliWealth is here to assist you throughout this journey, providing expert guidance to help you secure your future with confidence.

Embarking on the journey of retirement planning is a significant step towards securing your future. While this path may be long and requires careful navigation, remember that you're not alone. At SimpliWealth, we stand ready to be your dedicated companions throughout this journey.

As you navigate the complexities of retirement planning, we are committed to providing expert guidance, personalized strategies, and unwavering support. Your goals are our priority, and we take pride in helping you achieve them.

Rest assured, the road to a financially secure retirement is made smoother with the right guidance. Let us be a part of your success story. Contact us today, and together, we'll shape a retirement that's filled with comfort, dignity, and fulfillment.

Disclaimer

The information provided in this guide is for educational purposes only and does not constitute financial advice. Please consult with a qualified financial advisor before making any investment decisions.