General Elections 2024

Anticipating the Stock Market's Reaction to the Results

Sneha T - SimpliWealth

6/3/20243 min read

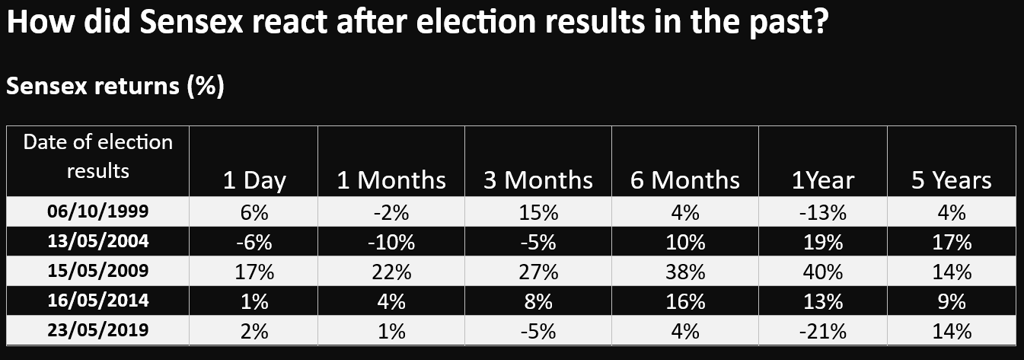

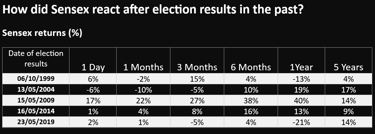

The stock market's reaction to the results of the General Elections in 2024 will hinge largely on whether the outcomes align with investor expectations. Historically, markets have shown significant short-term volatility following election results, but this volatility tends to level out over the longer term.

In the short run, the stock market can be extremely unpredictable. For instance, over the past decade, investing in the Sensex for just a single day resulted in negative returns 46% of the time. However, extending the investment period to five years significantly reduced the instances of negative returns to less than 0.5%. This trend is also evident in the market's reaction to election results.

Here are some guidelines to follow:

1. Invest for the Long Term: Aim to hold equities for more than five years to ride out short-term market fluctuations.

2. Stick to Your Plan: Do not alter your investment strategy based on short-term market movements, including those caused by-elections.

3. Avoid Market Timing: Refrain from making opportunistic bets or trying to time the market.

By maintaining a long-term perspective and staying committed to your investment plan, you can effectively manage the inherent volatility that accompanies election cycles and other significant events.

SIP Investment: A Proven Path to Long-Term Wealth Creation

Systematic Investment Plans (SIPs) have emerged as one of the most effective methods for building long-term wealth without disrupting day-to-day life. This innovative approach in the mutual funds industry promotes a disciplined and long-term financial strategy. By investing in equity mutual funds through SIPs, investors benefit from rupee cost averaging, which reduces the overall cost of holding investments over time. SIPs provide a stable financial vehicle to navigate market volatility.

Static SIP vs. Step-Up SIP

When comparing static SIPs to step-up SIPs, the primary difference lies in the pattern of monthly contributions. In a step-up SIP, the investment amount increases annually based on predefined parameters, such as a fixed sum or a fixed percentage.

For instance, if the step-up SIP percentage is set at 10% and the initial contribution in the first year is Rs.1000, the contribution would increase to Rs.1100 in the second year, Rs.1210 in the third year, and so on. In contrast, the monthly contribution in a static SIP remains constant throughout the investment period.

By adopting SIPs, particularly step-up SIPs, investors can enhance their investment strategy, steadily increasing their contributions over time to maximize returns and better manage their wealth.

Why Not Static SIP Investment?

The main drawback of a static SIP investment compared to a step-up SIP is that it does not account for an individual's increasing income-earning capacity. As a person's income grows over time, their savings should also increase accordingly. A step-up SIP addresses this by encouraging periodic increases in contributions based on one's financial capability. This approach ensures that investments grow in line with income, maximizing long-term wealth accumulation.

Step-Up SIP vs. Static SIP Investment

Step-up SIP accounts for inflation, which diminishes the value of money over time, making it prudent to increase investments periodically. Step-up SIP offers several advantages over static SIP investment, ensuring your investment grows alongside your income and preserves purchasing power.

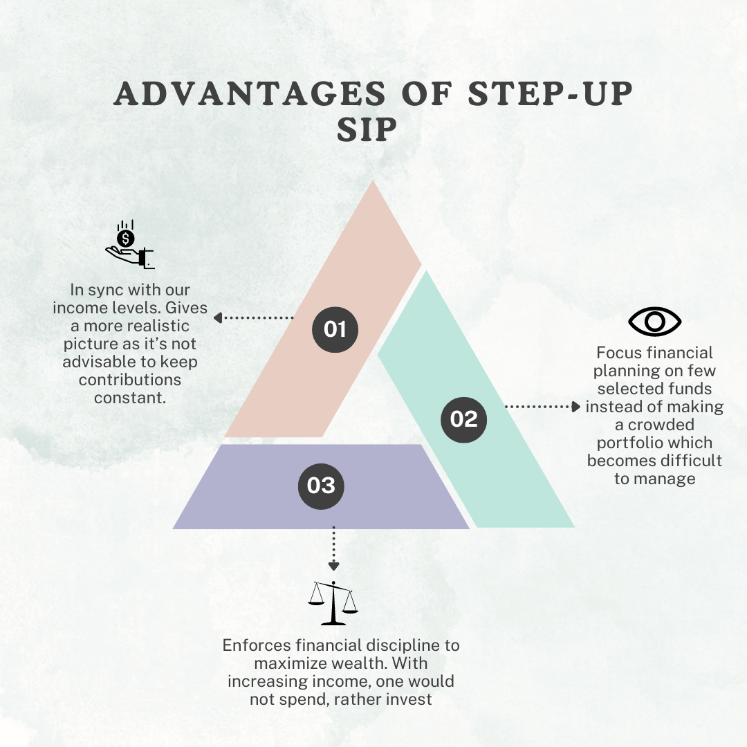

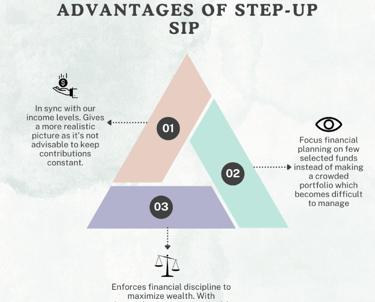

Does Step-Up SIP Perform Better?

Step-up SIP leverages the power of compounding, enabling investors to achieve their financial goals more quickly. Often, individuals fail to voluntarily increase their SIP contributions, neglecting to align their investment plan with their growing income. Step-up SIP addresses this issue by automatically increasing contributions, and promoting effective long-term wealth creation.

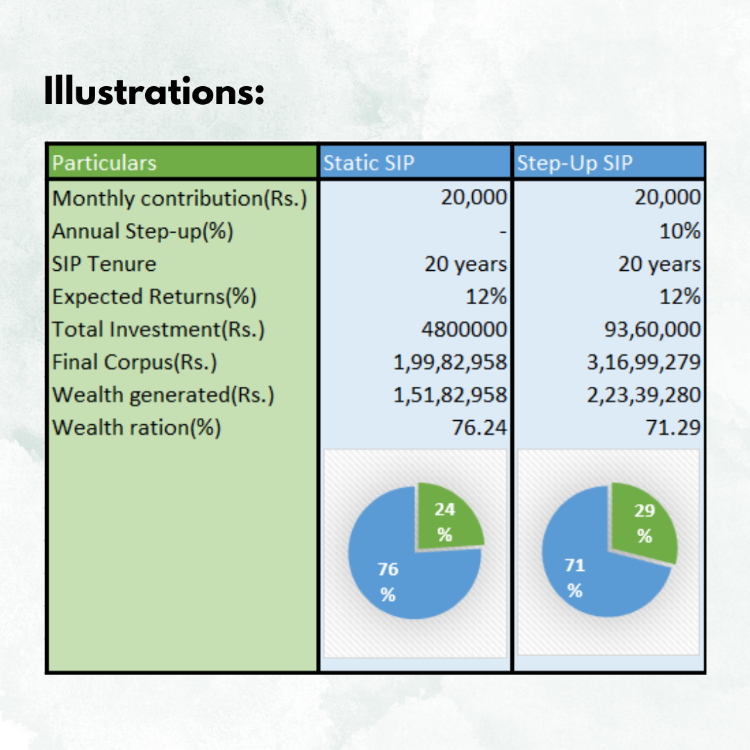

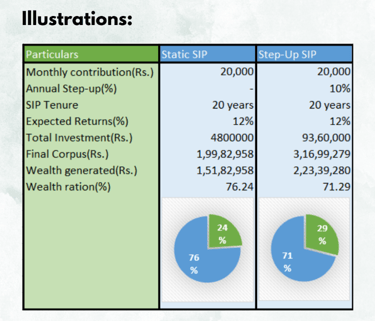

Now let’s take a look at the practical difference in returns between the two SIPs: